-

SHAPE M&V policy by serving on relevant committees

-

STAY CURRENT on the latest in M&V policy and practices

-

AFFILIATE with the foremost industry voice of measurement and verification

-

NETWORK with leaders in the industry

- 1

- 2

- 3

- 4

M&V

The fundamental principles of good M&V practice described below provide the basis for assessing adherence to IPMVP. These principles should be considered and applied throughout the M&V process.

Accurate

M&V Reports should be as accurate as can be justified based on the project value and goals. M&V costs should normally be “small” relative to the monetary value of the savings being evaluated. M&V expenditures should also be consistent with the financial implications of over- or under-reporting of a project’s performance. The M&V methodology’s accuracy and cost should be evaluated as part of the project development. Accuracy trade-offs should be accompanied by increased conservativeness with increased use of estimated values and assumptions based on sound engineering judgment. Consideration of all reasonable factors that affect accuracy is a guiding principle of IPMVP.

Complete

The reporting of energy savings should consider all effects of a project. M&V activities should use measurements to quantify energy use within the measurement boundary, document energy influencing factors, and detail any estimated values. By identifying key areas where judgment is required, IPMVP helps to avoid inconsistencies arising from a lack of consideration of important aspects.

Conservative

Where judgments are made about uncertain quantities, M&V procedures should be designed to reasonably estimate savings such that they are not over- or under-stated. An assessment of a project’s impact should be made to assure its energy-saving benefits are reasonable and conservative with due consideration to the level of statistical confidence in the estimation.

Consistent

The reporting of a project’s energy performance should be consistent and comparable across:

- Different types of energy efficiency projects

- Different energy management professionals for any project

- Different periods of time for the same project

- Energy efficiency projects and new energy supply projects

Consistent does not mean identical since it is recognized that any empirically derived report involves assumptions based on sound engineering judgment, which may not be made identically by all reporters.

Relevant

The determination of savings should be based on current measurements and information pertaining to the facility where the project occurs. This determination of the savings effort must measure the energy influencing factors and verify performance indicators that are of concern related to the EEM.

Transparent

All M&V activities should be clearly documented and fully disclosed. Full disclosure should include presentation of all of the elements of an M&V Plan and savings reports, and confirmation that the M&V Plan is agreed upon and understood by all stakeholders. Data and information collected, data preparation techniques, algorithms, spreadsheets, software, assumptions used, and analysis should follow industry standard best practices as closely as possible, be well formatted and documented – such that any involved party or independent reviewer can understand how the data and analysis conformed to the M&V Plan and savings reporting procedures. Transparency also means that any possible conflicts of interest are disclosed to all stakeholders in the project.

M&V techniques can be used by facility owners or energy efficiency project investors for the following purposes:

Increase energy savings

Accurate determination of energy savings gives facility owners and managers valuable feedback on their energy conservation measures (ECMs). This feedback helps them adjust ECM design or operations to improve savings, achieve greater persistence of savings over time, and lower variations in savings.

Document financial transactions

For some projects, the energy efficiency savings are the basis for performance-based financial payments and/or a guarantee in a performance contract. A well-defined and implemented M&V Plan can be the basis for documenting performance in a transparent manner and subjected to independent verification.

Enhance financing for efficiency projects

A good M&V Plan increases the transparency and credibility of reports on the outcome of efficiency investments. It also increases the credibility of projections for the outcome of efficiency investments. This credibility can increase the confidence that investors and sponsors have in energy efficiency projects, enhancing their chances of being financed.

Improve engineering design and facility operations and maintenance

The preparation of a good M&V Plan encourages comprehensive project design by including all M&V costs in the project’s economics. Good M&V also helps managers discover and reduce maintenance and operating problems, so they can run facilities more effectively. Good M&V also provides feedback for future project designs.

Manage energy budgets

Even where savings are not planned, M&V techniques help managers evaluate and manage energy usage to account for variances from budgets. M&V techniques are used to adjust for changing facility-operating conditions in order to set proper budgets and account for budget variances.

Enhance the value of emission-reduction credits

Accounting for emission reductions provides additional value to efficiency projects. Use of an M&V Plan for determining energy savings improves emissions-reduction reports compared to reports with no M&V Plan.

Support evaluation of regional efficiency programs

Utilty or government programs for managing the usage of an energy supply system can use M&V techniques to evaluate the savings at selected energy user facilities. Using statistical techniques and other assumptions, the savings determined by M&V activities at selected individual facilities can help predict savings at unmeasured sites in order to report the performance of the entire program.

Increase public understanding of energy management as a public policy tool

By improving the credibility of energy management projects, M&V increases public acceptance of the related emission reduction. Such public acceptance encourages investment in energy-efficiency projects or the emission credits they may create. By enhancing savings, good M&V practice highlights the public benefits provided by good energy management, such as improved community health, reduced environmental degradation, and increased employment

“Measurement and Verification” (M&V) is the process of planning, measuring, collecting and analyzing data for the purpose of verifying and reporting energy savings within an individual facility resulting from the implementation of energy conservation measures (ECMs). Savings cannot be directly measured, since they represent the absence of energy use. Instead, savings are determined by comparing measured use before and after implementation of a project, making appropriate adjustments for changes in conditions.

M&V activities consist of some or all of the following:

- meter installation calibration and maintenance,

- data gathering and screening,

- development of a computation method and acceptable estimates,

- computations with measured data, and

- reporting, quality assurance, and third party verification of reports.

When there is little doubt about the outcome of a project, or no need to prove results to another party, applying M&V methods to calculate savings may not be necessary. However, it is still wise to verify (initially and repeatedly) that the installed equipment is able to produce the expected savings. Verification of the potential to achieve savings is referred to as operational verification, which may involve inspection, commissioning of equipment, functional performance testing and/or data trending. IPMVP-adherent M&V includes both operational verification and an accounting of savings based on site energy measurements before and after implementation of a project, and adjustments.

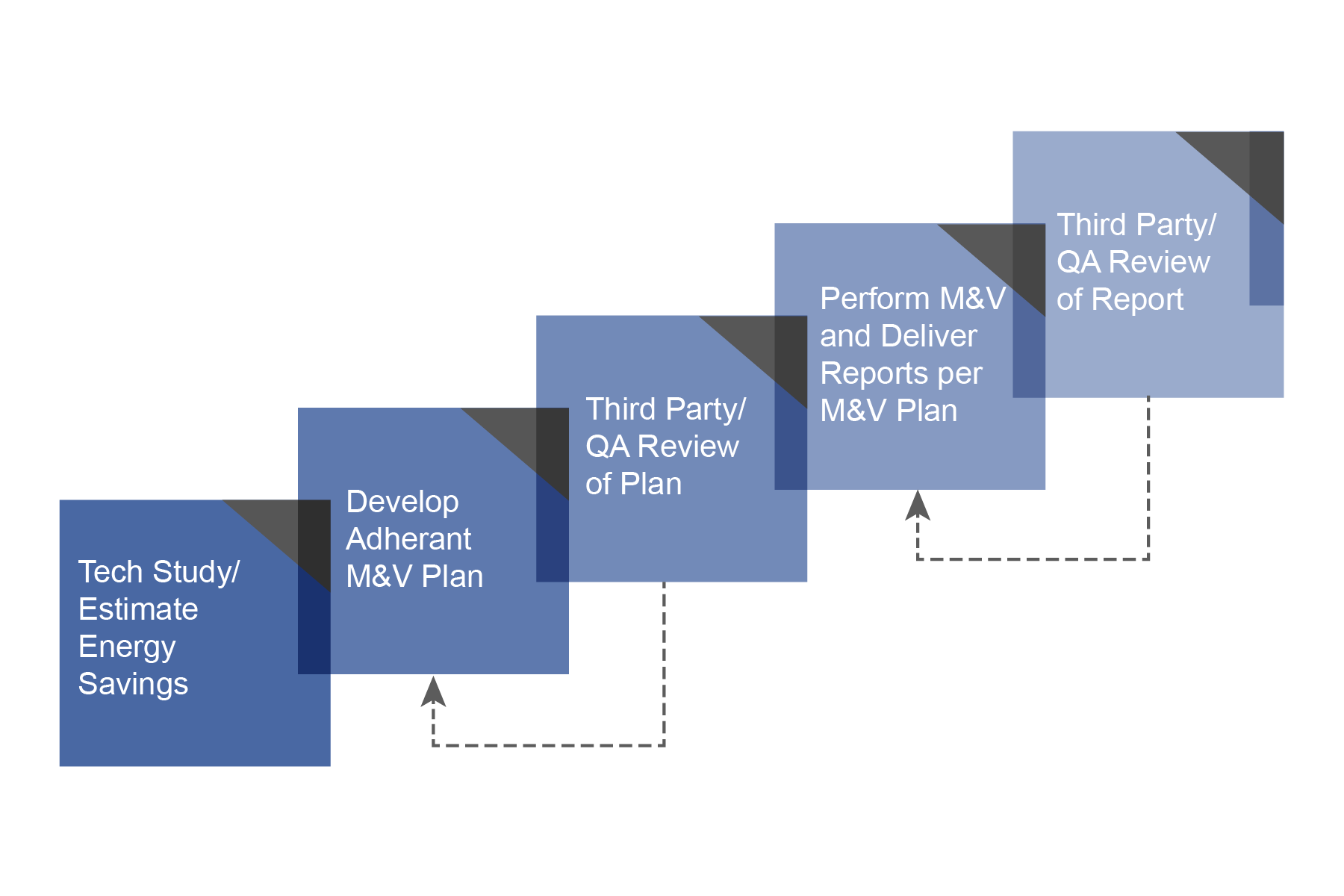

M&V is not just a collection of tasks conducted to help a project meet IPMVP requirements. Properly integrated, each M&V task serves to enhance and improve facility operation and maintenance of savings. As shown in the figure below, M&V activities overlap with other project efforts (e.g. collecting data to both identify ECMs and establish energy baselines, commissioning and operational verification of installed ECMs, and installing monitoring systems to track and maintain savings persistence, etc.). Identifying these project synergies and establishing roles and responsibilities of involved parties during project planning will support a coordinated team effort. This can leverage complementary scopes and control M&V-related costs.